.png)

By Dhananjay Sinha

Dhananjay Sinha, CEO and Co-Head of Institutional Equities at Systematix Group, has over 25 years of experience in macroeconomics, strategy, and equity research. A prolific writer, Dhananjay is known for his data-driven views on markets, sectors, and cycles.

September 16, 2025 at 7:53 AM IST

India’s household economy is showing tentative signs of recovery after a strong monsoon season. The revival, however, remains fragile, driven more by easing inflation than by income growth.

Rural demand, long the cornerstone of India’s consumption story, is flickering back to life, supported by government interventions, GST reform, and the promise of festive-season tailwinds.

Urban sentiment, by contrast, remains subdued. Discretionary spending continues to trail pre-COVID levels, while structural income weaknesses threaten to cap momentum.

Taken together, the mix of rural and urban consumption trends, agricultural output, consumer confidence, corporate behaviour, and policy measures points to cautious optimism—tempered by deep underlying vulnerabilities.

Rural Demand

India’s rural economy, home to more than 65% of the population, is showing a tentative consumption uptick, but the recovery feels more like a pause than a structural shift.

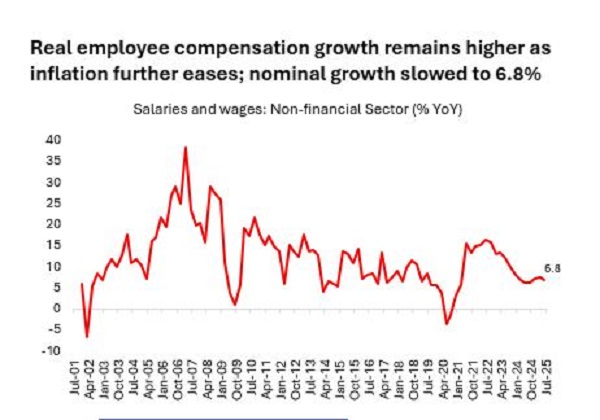

Real rural wages rose 4% year-on-year in July 2025, the strongest increase since 2017 following prolonged stagnancy, helped by rural inflation falling to just 1.7%. Nominal wage growth, however, stayed steady at 6%, suggesting the boost may prove fleeting if inflation re-accelerates. MGNREGA data reflects this fragility: real wages dropped to 4.7% in July from 9.8% in June.

NABARD’s rural surveys highlight deeper cracks. In July, 39.6% of households reported income growth, up from 34.8% in March. Yet, better-off segments, those reliant on diversified activity or urban remittances, saw incomes decelerate, increasing dependence on government transfers.

Spending patterns also underline the strain. While 76.6% of households reported higher outlays, down from 80% in March, savings fell to 13.2% of monthly income from 13.8%, pushing the consumption-to-income ratio up to 65.6%.

Food’s share of expenditure hit a record 53.8%, crowding out education and health, which fell to 22.3% from 24.5% a year ago. Informal borrowing rose to 20.5% of households from 17.7% in March, pointing to tighter credit and a shift away from formal lending. Without sustained wage growth, the apparent recovery in rural purchasing power, and the consumer goods demand it fuels, risks fading quickly.

The 2025 monsoon has been bountiful, coming 11% above the long-period average and marking the earliest onset since 2009. Kharif sowing has expanded by 6.1%, reservoir levels are healthy, and tractor sales are up 7.8% year-to-date, a sharp rebound from just 0.1% last year. Still, July’s growth slowed compared to February’s 32% peak, reflecting base effects.

Yet, the benefits may not translate into meaningful income gains. Wheat mandi prices have stayed subdued for months, and wholesale price inflation for primary food articles has been contracting since April. Even with a bumper harvest, stagnant prices suggest only modest improvements in farm incomes, reinforcing the point that disinflation, rather than structural gains, is driving rural recovery.

Rural vs Urban

RBI’s bi-monthly surveys reveal a widening divergence. In rural areas, the share of households reporting economic improvement rose to 7.1% in July from 6.9% in May, helped by seasonal farm activity. Income pessimism narrowed to −3.1% from −4.8%, though 45% of households continue to report stagnant incomes since September 2023. Essential spending dipped to 87% from 88.1%, while non-essential spending rose to 37.2% from 35.2%, aided by lower prices.

Urban India remains stuck in pessimism, marking 12 consecutive months of negative confidence. Views on employment slipped to −6.7%, worse than the 12-month average of −7.2%, and 56.7% of households reported stagnant incomes, the highest since 2012. Yet spending held up: 78% reported higher outlays, with discretionary spending jumping to 37.6% from 27.8%, thanks to easing price pressures.

PwC’s Voice of the Consumer 2025 report reinforces the strain: only 60% of respondents feel financially secure, while 40% are struggling, relying on discounts and store switching.

PLFS data shows unemployment easing to 5.2% in July from 5.6% in June, driven by rural declines, even as urban unemployment rose to 7.2%. Labour force participation ticked up to 54.9%, but youth unemployment remains high at 14.9%, reflecting seasonal agricultural absorption and disguised, low-productivity jobs rather than genuine employment creation.

Corporate vs Government

Government spending is offering a cushion. Central real revenue expenditure excluding interest grew 3.9% in April–June 2025–26, compared with just 0.1% in 2024–25, providing crucial rural support.

GST rate rationalisations, with an estimated ₹480 billion revenue hit or 0.2% of nominal private consumption, aim to ease household burdens and spur demand. Cuts on essentials such as food, health drugs, automobiles, and farm equipment, alongside higher levies on luxury and sin goods, could boost consumption, though weak incomes may cap volumes. Organized players are likely to gain pricing power as supply chains normalise.

Consumer Sector Muted

Discretionary segments showed mixed signals. Passenger vehicle sales grew 1.5% year-on-year in July, MUVs up 2.4%, two-wheelers surged 13.3%, premium bikes 21.7%, but entry-level cars slipped. AC sales rose 8.1% in April with a five-year compound annual growth rate of 4.4%, still below the pre-COVID average of 9%. Refrigerators gained 4.6%, with a CAGR of 1.4%.

Bank retail lending slowed to 12% year-on-year, though jewellery loans spiked 122%, signalling financial stress. Household net financial savings recovered modestly, up 1.2% year-on-year in January–March 2025, as liabilities fell faster than financial assets.

A Fragile Inflection Point

Consumer goods firms are reporting slightly better rural traction, but its sustainability is uncertain without stronger wage gains. The divergence is stark: headline GDP data shows real private consumption growth above 7%, yet household surveys reveal persistent pessimism. The gap between aggregate numbers and lived realities highlights the fragility of the recovery.

Investors will be watching the second half of the year for evidence of a more durable turnaround. For now, India’s consumption story remains one of cautious hope, undercut by structural vulnerabilities.

More From BasisPoint