.png)

Venkat Thiagarajan is a currency market veteran.

April 14, 2026 at 2:22 PM IST

“Few issues in economics are more susceptible to political misrepresentation than exchange rates.” - Niall Ferguson

Exchange rate movements are deeply embedded in macroeconomic conditions, which makes it genuinely difficult to isolate their effects. This is the classic endogeneity problem in econometrics: exchange rates are not exogenous shocks but part of a system of simultaneous equations. Despite the potentially significant policy implications of globalisation-related shifts in the exchange rate-economy relationship, the empirical evidence remains scarce and fragmented across economies.

History offers ample demonstration that exchange rate fluctuations do not occur in isolation. They transmit through both real and financial channels, shaping economic activity in ways that standard models often understate.

The overall evidence on structural changes in the size of exchange rate shocks is mixed, but the direction of the effects and the channels through which they operate have become clearer over time.

The effect on trade is one of the most studied questions in international economics, yet the theoretical answer remains unsettled. Standard open-economy models suggest that depreciation should be expansionary because it improves the competitiveness of domestic exporters. Models incorporating financial frictions, however, reach the opposite conclusion: when borrowers carry foreign currency liabilities that are not fully hedged, currency depreciation can be contractionary. These two opposing forces make it difficult to establish causality and point to very different policy conclusions.

Trade Channel

The conventional view is that a weaker domestic currency should lift exports and dampen imports, supporting growth through expenditure switching. That intuition still underpins much of the policy and market thinking around depreciation as a growth lever.

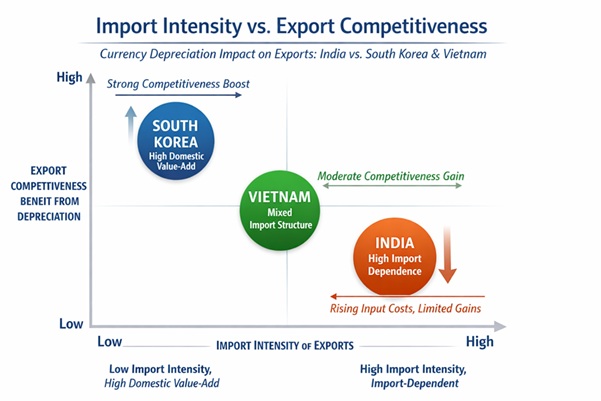

The Marshall-Lerner condition provides a theoretical lens: devaluation improves the trade balance only if the combined price elasticity of imports and exports exceeds one. In India’s case, this threshold is rarely met in practice. Imports are deeply embedded in the export production process, which means the scope to compress import demand is limited. At the same time, rising input costs tend to erode export margins well before any volume gains meaningfully show up.

India’s export competitiveness, therefore, is shaped less by currency moves and more by structural factors such as supply chain resilience, productivity and global demand conditions. In that context, depreciation can work against exporters when imported inputs dominate the value chain.

It is also worth noting that economic agents do not react sharply to small currency moves. Adjustment costs, contracts and hedging behaviour tend to dampen the immediate response. Larger shocks, however, are a different story. They force adjustment and often trigger disproportionately stronger reactions. If exchange rate volatility rises over time, the economic impact of these moves can become more pronounced than policymakers anticipate.

Financial Channel

In theory, changes in the exchange rate have two opposite effects on investment. Capital inflows tend to push up the domestic currency, lifting the apparent profitability of investment, especially in the non-tradable sector where revenues are not naturally hedged in foreign currency. As balance sheets strengthen, firms find it easier to borrow, credit expands and a familiar cycle takes hold: inflows, appreciation and rising investment feeding into each other.

However, a shift in global liquidity, a terms-of-trade shock or even a policy misstep can reverse flows quickly. The currency weakens, balance sheets come under pressure and credit conditions tighten. The same dynamics that supported growth on the way up begin to drag on activity on the way down.

The risks become sharper when non-financial corporates borrow in foreign currency without adequate hedging. Much of this borrowing is often done on the assumption that the domestic currency will remain stable or continue to strengthen. Experiences across Latin America and parts of Central and Eastern Europe show how currency mismatches can turn depreciation into a contractionary force.

Formal models, including those of Krugman (1999), Aghion et al. (2000, 2004), and Céspedes et al. (2003, 2004), capture this mechanism by linking currency mismatches with financial frictions. As balance sheets deteriorate during a depreciation, the contraction in credit reinforces and extends the initial shock.

Where foreign exchange markets are shallow, hedging instruments are limited and costly. Effective hedging becomes impractical for most corporate borrowers, and currency mismatches persist on balance sheets. The capacity to borrow or lend then becomes tightly linked to net worth, which is itself a function of the exchange rate. This feedback loop makes external financing conditions and exchange rate dynamics inseparable, something traditional open-economy models do not adequately capture.

For example, it is possible that economic agents do not respond strongly to relatively small changes in exchange rates, reflecting, among others, adjustment costs. By contrast, larger exchange rate shocks may trigger a disproportionately larger response, as agents are willing to incur the adjustment costs. If, in such a situation, the volatility of exchange rates, and thus presumably the size of exchange rate shocks, increases over time, this would result in exchange rate changes having a stronger effect on economic variables.

There is meaningful heterogeneity across firms, however. Those that both import and export are partly hedged through their revenue structure, particularly when export revenues are priced in foreign currency. Firms holding foreign currency assets are also insulated from debt revaluation effects. And those using derivative contracts do not face the same balance sheet stress during a depreciation episode. The aggregate contractionary effect, therefore, depends significantly on the composition of the corporate sector and the depth of the hedging market — neither of which is static.

Whether depreciation is ultimately contractionary or expansionary depends on which channel dominates. The trade channel's strength varies with the nature and composition of trade flows; the financial channel's intensity depends on the sensitivity of domestic balance sheets to exchange rate movements and the volume of unhedged foreign borrowing. Both differ substantially across countries, which is why the same depreciation can boost growth in one economy and drag it down in another.

Any meaningful debate on exchange rates has to be grounded in the broader economic context. The East Asian economies that sustained high growth through currency undervaluation also maintained credible microeconomic frameworks that promoted export-oriented industrialisation. In several cases, there were explicit policies to keep the prices of capital goods and wage goods (including food) low, as a counterweight to the income effects of a weaker currency. Without those complements, using the exchange rate as a growth instrument carries risks that are frequently underestimated in the policy discourse.

Policy Reality

For India specifically, the conventional narrative of depreciation-led export competitiveness is misleading. The export basket is tightly linked to imports, from petroleum and gems to electronics and pharmaceuticals. A weaker rupee raises the cost of these inputs, squeezing margins and diluting whatever price advantage exports might gain. Depreciation does not translate straightforwardly into improved competitiveness; instead, it transfers costs upstream into the production chain.

On the financial side, India's corporate sector carries a meaningful stock of foreign currency borrowing, not all of it well-hedged. A sharp depreciation raises the rupee value of these liabilities, weakens balance sheets and curtails the ability of firms to invest. It can also trigger a pullback in credit that spills beyond the most exposed borrowers into the wider economy.

The monetary policy trade-off is equally uncomfortable. As depreciation feeds into higher import prices, the central bank is forced to balance currency stability against growth, with little room to fully support either.

The conclusion that follows is not a comfortable one for policymakers drawn to exchange rate targeting as a shortcut. When the trade channel is muted by import dependence and the financial channel amplifies balance sheet stress, depreciation functions less as an engine of competitiveness and more as a source of contraction.

The assumption that a weaker rupee will always be net-positive for the economy — still present in much of the public debate — is one that the evidence does not support. That is the empirical record India needs to reckon with.

BasisPoint Briefing — Explainers from seasoned practitioners for readers who want more than the basics.

More From BasisPoint