.png)

By R. Gurumurthy

Gurumurthy, ex-central banker and a Wharton alum, managed the rupee and forex reserves, government debt and played a key role in drafting India's Financial Stability Reports.

September 16, 2025 at 9:01 AM IST

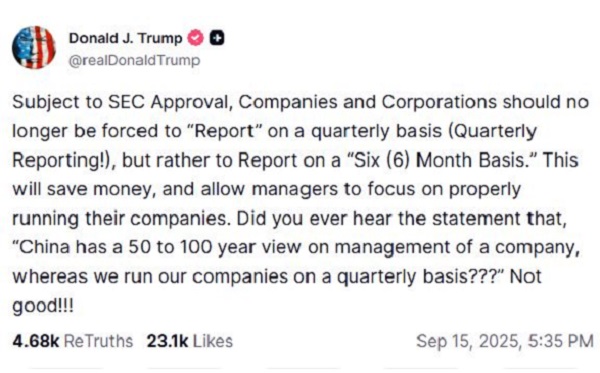

When Donald Trump announced on Truth Social that US companies should report earnings every six months instead of quarterly, sceptics may have dismissed it as another populist provocation. Yet this was no stray thought, since Trump had first floated the idea in 2018 and has now, in September 2025, returned to it as a regulatory priority. According to media reports, the US Securities and Exchange Commission is reviewing the proposal.

Trump’s intervention has revived the long-running debate over what critics call “quarterly capitalism”. Every three months, corporate America submits to a ritual: numbers flash, guidance shifts, and CEOs either emerge as conquering heroes by beating “the Street” by a cent or disgraced villains by missing by a whisker. Miss a quarter and billions are lost; meet expectations and the firm survives another three months; beat them and perhaps hedge funds grant six months’ respite.

Into this cycle steps the Long-Term Stock Exchange or LTSE, founded by Eric Ries, author of The Lean Startup. Unlike Trump’s blunt proposal, LTSE is building a parallel system. Its pitch is that companies and investors should think in decades rather than quarters, and it has petitioned the SEC to consider abolishing quarterly earnings reporting altogether, a direct challenge to the cadence of American capitalism.

Critics argue that the obsession with near-term earnings undermines investment in innovation, infrastructure, and people. Why spend on R&D if analysts punish a temporary dip in margins? Why pursue long-horizon strategies if missing consensus by two cents invites activist hedge funds to demand a resignation?

Warnings against short-termism have come even from titans of finance: in 2018, Warren Buffett and Jamie Dimon urged companies to abandon quarterly guidance, saying it was hurting the economy. Europe scrapped mandatory quarterly reporting in 2013, and Japan has encouraged stewardship codes to nudge investors toward patience. Yet the United States remains bound to its 90-day treadmill.

That is why Trump’s call matters. For once, a populist president and a Silicon Valley start-up exchange are pushing in the same direction by questioning the cultural and financial tyranny of quarterly disclosure.

LTSE’s Bet

The LTSE aims to institutionalise what CEOs solemnly claim on every call: that they are focused on the long term. Its listing rules require boards to align pay with long-run success rather than quarterly EPS. Companies must explain how they prioritise innovation, governance, human capital, and sustainability. LTSE also encourages mechanisms such as loyalty shares, extra rights for long-term shareholders, or tenure-based voting to benefit patient capital, though trading itself remains unrestricted.

Its most radical step is the bid to roll back quarterly earnings altogether. Where Trump seeks a regulatory shortcut by halving reporting frequency, LTSE is trying to construct a sanctuary for patience.

The vision is seductive: imagine a biotech firm freed from quarterly comparisons, able to pursue decade-long research without being punished for years of losses; imagine Tesla judged not on deliveries this quarter but on its 20-year bet on energy storage.

Yet scepticism runs deep. Liquidity is the lifeblood of exchanges, fuelled by traders feeding on volatility and near-term catalysts. Why migrate to a venue that denies them their favourite meal? Companies, too, crave prestige and depth, which still lie with Nasdaq and the NYSE. LTSE’s listings remain thin, and its volumes are thinner, a reminder that nobility rarely pays dividends.

Trump’s plan, meanwhile, faces political as well as financial pitfalls. Quarterly reporting was born of the 1934 Securities Exchange Act, designed during the Great Depression to restore investor trust. The SEC’s Form 10-Q, adopted in 1935, gradually became mandatory for nearly all public firms by the 1970s. Rolling it back risks charges of opacity, a dangerous move in an era of populist distrust, and Trump’s role as messenger may further complicate adoption.

Reform to Ritual

The irony is historical. Quarterly reporting began as a reform meant to protect investors, but ninety years later, the cure feels like a disease. More disclosure has produced not clarity but noise. Analysts slice forecasts to the cent, algorithms trade in microseconds, and executives massage numbers to “meet the Street”. The result is a hyper-transparent yet strangely myopic market.

There is global evidence to suggest that alternatives are possible. Europe’s 2013 decision to end mandatory quarterly reporting did not trigger a collapse. Some firms still report quarterly, others slowed the rhythm, and markets adjusted. Japan’s governance reforms under Abenomics nudged companies toward longer horizons through its Stewardship Code and Corporate Governance Code. Results are mixed, but the cultural tempo shifted.

America continues to cling to its quarterly confessional. Analysts, traders, and pundits depend on the steady drip of numbers. Politically, retreat from disclosure remains radioactive. Yet the fact that both a start-up exchange and a president are pushing slower rhythms signals that the debate is no longer unthinkable.

Viewed satirically, the LTSE is both thrilling and quixotic: thrilling because it challenges capitalism’s default settings — must our lives be organised into 90-day sprints? quixotic because it assumes investors conditioned to salivate at earnings beats can suddenly savour decade-long strategies. The contrasts write themselves. On the NYSE, traders scream at Bloomberg screens; on the LTSE, monks chant EBITDA projections for 2040 in Gregorian harmony; at Mar-a-Lago, Trump resets the calendar with a 180-day clock.

Yet the realities of market behaviour intrude quickly. CEOs dread illiquidity, pension funds prefer depth to desert, and executives struggle to resist the dopamine hit of beating consensus. Even so, it would be too easy to dismiss both the LTSE and Trump’s idea outright. Their existence raises a deeper question: can capitalism be rewired to reward patience, or is short-termism the system’s operating code?

If LTSE fails, it may be because quarterly capitalism is too entrenched. If Trump’s proposal stalls, it may be because Wall Street prefers the drip feed of numbers. Yet even failure serves a purpose by reminding us that market rules are human constructs rather than natural laws. Quarterly reporting itself was once an innovation; its replacement could be one too.

The LTSE may never rival Nasdaq or the NYSE. Its ideals may be mocked, and Trump’s plan may dissolve into another half-kept promise, but both deserve a hearing. Everyone complains about short-termism, and at least someone is trying to change the channel. If quarterly earnings are capitalism’s reality TV show, the question now is what happens if we simply turn off the cameras, or at least dim the lights.

More From BasisPoint