In its June 2026 policy meeting, the Reserve Bank of India left the repo rate and stance unchanged despite acknowledging heightened geopolitical uncertainty and upside risks to inflation. Instead, it unveiled a host of measures to encourage capital flows, focusing on non-resident Indians, while reiterating that future policy directions would remain data dependent.

However, it seems, the policy decision was mostly based on hope rather than reality. For example, as per the minutes of the meeting, one Monetary Policy Committee member noted that risks could ease if food inflation remains stable, global crude oil prices stabilise below $80 per barrel and the US Federal Reserve avoids a more hawkish stance. In the meantime, CPI headline inflation in May 2026 surged to 3.93%, up 45 bps from the previous month, while WPI inflation shot up to 9.68%.

Against this backdrop, three issues merit closer examination. First, can measures aimed at attracting NRI capital compensate for the absence of interest rate increases if developed market rates continue to rise? Second, is the argument that the rupee at 100 “just a number” economically meaningful? Third, does intervention really reduce volatility in the markets?

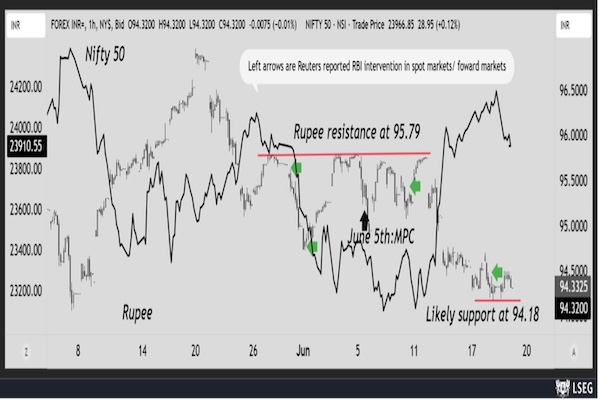

Chart 1: Rupee movement and reported intervention

Source: LSEG

The European Central Bank meeting that followed on 11 June, 2026, saw it raising its key policy rate by 25 basis points, the first increase since 2023, keeping in view the inflationary pressures from geopolitical tensions and energy prices (Reuters, 11 June 2026). Bank of Japan raised the policy rate to 1.0%, the highest level since 1995 (Reuters, 16 June, 2026). The US Federal Reserve meeting on 16–17 June kept rates unchanged, but maintained a hawkish stance given the overriding inflationary signals coming from the US real sector. Among 19 FOMC members, nine members are anticipating rate hikes during this year to combat inflation (Reuters, 17 June, 2026). In this scenario, will new measures work? And what would be the long-term impact?

In keeping with the success of the 2013 FCNR(B) measures, the Reserve Bank of India has announced a revamped FCNR(B) scheme to attract capital flows. Even conservative estimates put the amount of capital that can flow in at $20 billion and optimistic range anywhere between $35 billion to $40 billion. The maturity period for these deposits is of three to five years, and RBI will be bearing the full foreign exchange hedging cost for the same.

The questions are many. First, if in developed countries the interest rates start rising, will the FCNR(B) scheme be as lucrative? Second, even when RBI is bearing the hedging cost, what is the expected outflow from the Indian economy when the deposits mature?

While hedging allows us to lock in the dollar outflows, a depreciation of the rupee in the future, which is likely, would mean that every dollar of outflow in the future require more rupees to fund it. This in turn, would lead to an increase in money supply domestically, leading to inflation. Given the present geopolitical situation, the trajectory of oil prices is likely to continue on the upside, such that the resulting outflow of dollars and the likely increase of money supply internally can lead to extensive inflationary pressures.

Right now, RBI uses the forward market to balance the spot-side intervention, leading to build up of dollar liabilities in future which basically means that the central bank is promising dollar supply in the future. Already, concerns on the RBI’s short dollar book are evident. The short dollar book of the central bank has ballooned to an all-time high of nearly $110 billion, following continuous spot and forward interventions. This position will be expanded as banks pass on the currency risk of FCNR(B)-led inflow to RBI through hedging.

This will not only keep the depreciating pressures on rupee, but also require the central bank to buy dollars to build up the reserves, as we saw recently. The buying of dollars leads to increase in rupee liquidity, leading to inflationary pressures; as does the build of dollar liabilities in future, as it presupposes the build-up of dollar reserves. However, it is crucial to note that the problem is not just that increasing dollar reserves are expected in the future: every depreciation of the rupee means that those dollar flows have to be compensated by more rupees internally. In a country with a historically high inflation, such a policy is concerning. The future dollar liabilities baton is, in the meanwhile, passed on from one regime to another.

A second concern is India’s GDP in dollar terms falls sustainedly due to depreciation. Even as the RBI intervenes to smooth currency movements, policymakers have argued that the rupee remains competitive, and that an exchange rate of 100 per dollar should not be viewed with alarm.

However, rupee at 100 means India falls short of being a $4 trillion economy. With nominal GDP estimated at ₹357.14 trillion, an exchange rate of ₹95 per dollar translates into an economy worth roughly $3.76 trillion. At 100 per dollar, the figure falls closer to $3.5 trillion. On one hand, we are committing through intervention to greater dollar reserves in the future, and on the other hand our GDP, through depreciation, slips in dollar terms.

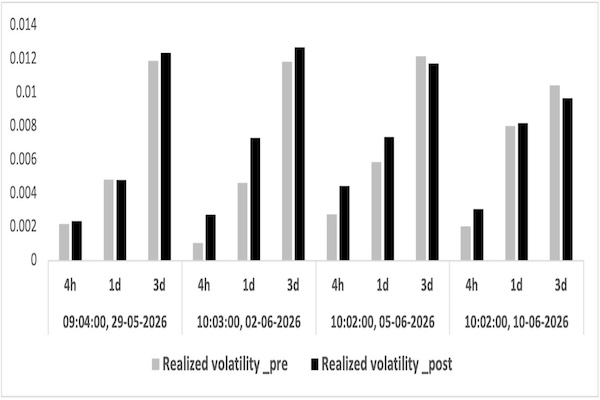

Finally, does intervention really lead to sustained lower volatility? Over what time frame and compared to what? The central bank has not provided any clarity on the same. There is limited evidence that intervention can alter exchange rate trends and reduce volatility.

For example, a quick check on the interventions reported in recent weeks suggests that intervention has had only a modest impact on realised volatility (Chart 2). However, as Chart 1 shows, an upper resistance has been maintained at 95.79. If the RBI does not target any particular exchange rate, how should market participants interpret the persistence of such support and resistant levels?

Greater transparency would help clarify both objectives and effectiveness of intervention. Without it, the distinction between volatility management and exchange rate management becomes increasingly blurred.

Taken together, recent policy actions suggest the RBI has chosen to depend on capital inflows and forex interventions rather than higher interest rates to support the rupee and manage external pressures.

Given the domestic liquidity repercussions of intervention and evidence of inflationary pressures building up, will this strategy prove to be a policy gamble?

Chart 2: Realised volatility for pre and post intervention events (May- June 2026)

Raw data Source: LSEG, Authors’ calculations; Note: #Realised volatility: square root of the sum of squared one-minute log returns over symmetric pre- and post-event windows of 240 (4-hour), 1,440 (1-day), and 4,320 (3-day) observations.

^ Post-event windows for 5 June and 10 June, 2026, contain 3,670 and 2,563 observations, respectively, instead of 4,320.

*Intervention events taken are based on Reuters reports, with the nearest market observation taken where exact timestamps are unavailable. In the absence of direct data from the central bank, this is closest proxy of intervention events timestamps. There is no report of intervention on 5 June, and is included on account of MPC announcement.

*Views are strictly personal

.png)