.png)

Dhananjay Sinha, CEO and Co-Head of Institutional Equities at Systematix Group, has over 25 years of experience in macroeconomics, strategy, and equity research. A prolific writer, Dhananjay is known for his data-driven views on markets, sectors, and cycles.

March 27, 2026 at 6:33 AM IST

Markets have responded to each turn in the conflict between the US and Iran with familiar reflexes, risk-off on escalation, relief rallies on talk of a pause. That pattern suggests markets are still conditioned to treat geopolitical shocks as transient events. The problem is that this shock is not cyclical but structural.

What is unfolding is not merely another West Asia flare-up, but a structural shift in the global order. The balance of economic and military power is shifting, alliances are fragmenting, and the institutional anchors of the post-World War II system are weakening. The current conflict has accelerated these dynamics.

Yet markets continue to price outcomes as though the system will revert to a pre-conflict equilibrium. That assumption looks increasingly untenable.

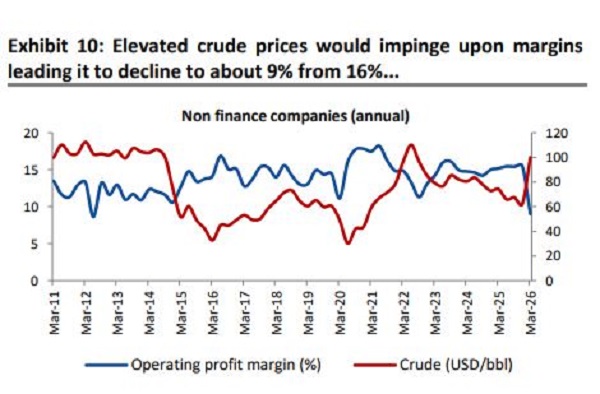

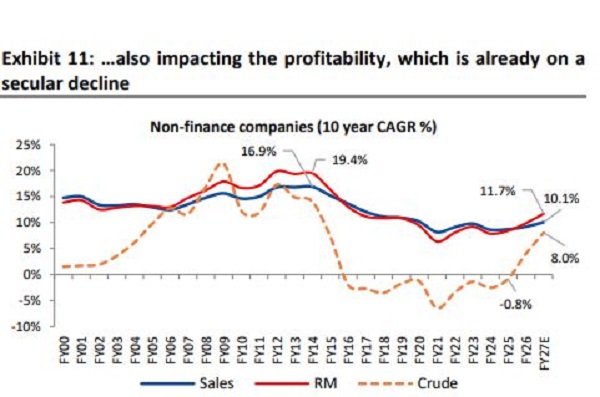

The first channel of mispricing lies in the energy sector. Oil is still treated as a volatility spike when it is more plausibly a regime shift. Disruptions around the Strait of Hormuz have already embedded a geopolitical risk premium into crude, with prices moving toward $100 per barrel. Even in a de-escalation scenario, infrastructure damage, supply realignments, and strategic behaviour by producers suggest that prices are unlikely to normalise quickly.

This matters because oil is no longer just an inflation variable; it is a macro anchor.

Persistently elevated energy prices feed into inflation expectations, fiscal balances, and current account dynamics. The result is a higher baseline for global risk-free rates and a compression of valuation multiples that markets have only begun to reflect.

The second channel is defence spending.

Since 2016, global military expenditure has been on a steady upward trajectory, with a clear acceleration in recent years. Governments are no longer responding to isolated threats; they are reorienting toward sustained deterrence.

That shift reallocates fiscal space away from growth-enhancing expenditure and locks in structurally higher borrowing. In a world already burdened with record debt, this reduces the capacity for counter-cyclical policy responses. Unlike the post-2008 or post-pandemic periods, there is limited room today for large-scale fiscal or monetary offsets.

Trade Fragmentation

For markets, this implies a steady erosion of the efficiency gains that underpinned globalisation. Supply chains become costlier, capital allocation more political, and cross-border flows less predictable. The cumulative effect is a structurally higher risk premium on global assets.

Taken together, these forces point to a world where volatility is not episodic but persistent, and where the equilibrium itself is shifting. Yet asset prices, particularly in equities, still appear anchored to a framework of mean reversion, where shocks fade and policy support restores stability.

Recent market behaviour offers early signs of adjustment. Indian equities have seen valuation compression, with foreign portfolio investors turning consistent sellers. Domestic flows have provided some cushion, but participation is becoming more concentrated, suggesting fragility beneath the surface.

Bond markets are sending a clearer signal. Yields have remained firm despite monetary easing, reflecting inflation persistence, fiscal concerns, and elevated term premia. This is not the response one would expect if markets believed the current shock to be temporary.

The central policy challenge is that traditional stabilisation tools are less effective. Monetary policy faces a narrower trade-off between inflation and growth, while fiscal policy is constrained by elevated debt and rising borrowing costs. The capacity to look through shocks is diminishing.

For investors, the implication is straightforward but uncomfortable.

Geopolitics is no longer a tail risk that can be discounted between episodes. It is becoming a core driver of macro and market outcomes.

The adjustment to this reality is unlikely to be abrupt. Markets tend to recognise regime shifts gradually, through a sequence of repricings rather than a single correction. The risk lies not in headline volatility, but in the slow recalibration of expectations as the structural nature of the shift becomes harder to ignore.

More From BasisPoint