.png)

Will RBI Bite the Bullet or Kick the Can Down the Road, Again?

As inflation risks mount and the rupee weakens, questions grow over whether the RBI delayed policy action despite warning signals.

Dr. Abhiman Das is a Professor of Economics at the Indian Institute of Management Ahmedabad.

Dr. Smita Roy Trivedi is an Associate Professor at the National Institute of Bank Management (NIBM), Pune.

May 27, 2026 at 7:52 AM IST

The RBI may be finally staring at a policy turn it has tried to avoid. With inflation pressures building, the rupee weakening sharply, import costs rising, and geopolitical disruptions intensifying, the case for tighter monetary policy has become difficult to ignore. While the April monetary policy seemed an opportune time to raise interest rates given a sharply depreciating rupee and early inflationary signals, the central bank chose to keep both, the rate and stance unchanged, with all members in agreement. Did the central bank miss seeing around the bend? Will missing the signals that were already visible in the economy entail a cost? A deeper concern is whether warning signs of emerging risk, which the central bank’s monetary policy is required to identify, were adequately recognised, interpreted, and incorporated into policy decision-making.

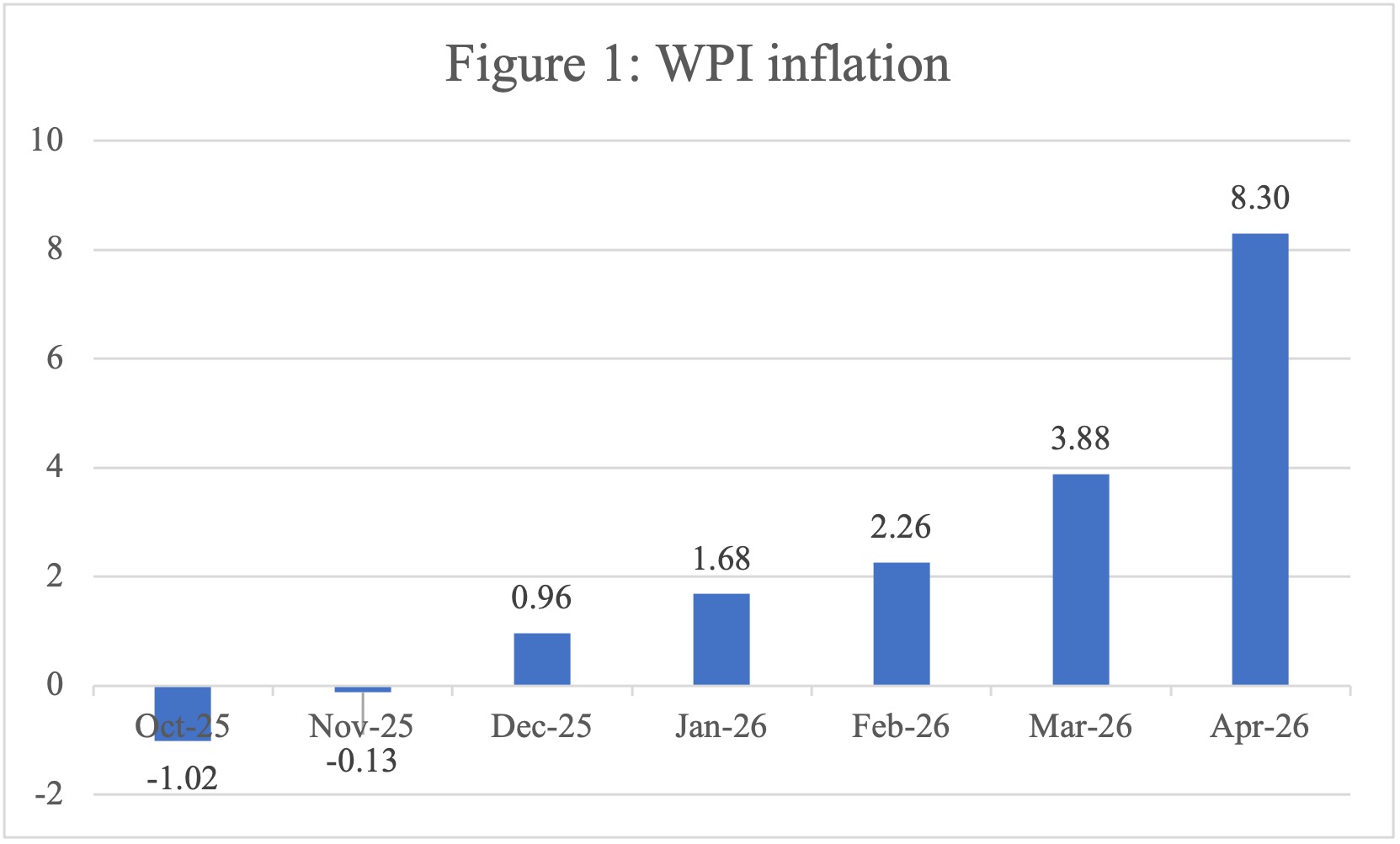

The present data reinforces these trends. WPI inflation rose to a 42-month high of 8.30% in April 2026, up sharply from 3.88% in March (Figure 1), an absolute increase of 4.42 percentage points in a single month. This is simply unprecedented and has not been witnessed in the past two decades.

Source: Office of Economic Advisor, DIPP

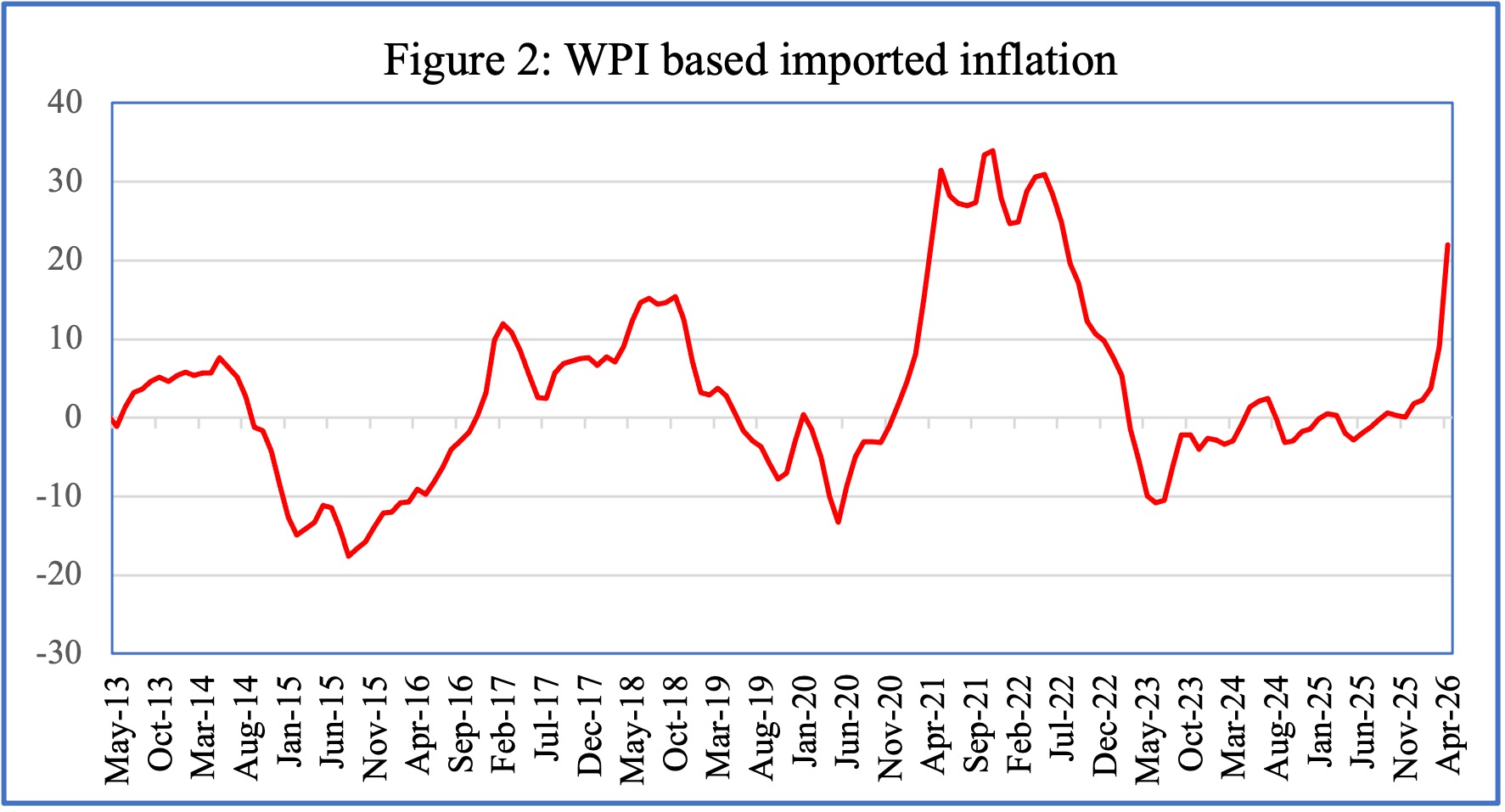

Source: Office of Economic Advisor, DIPP, Authors’ calculations

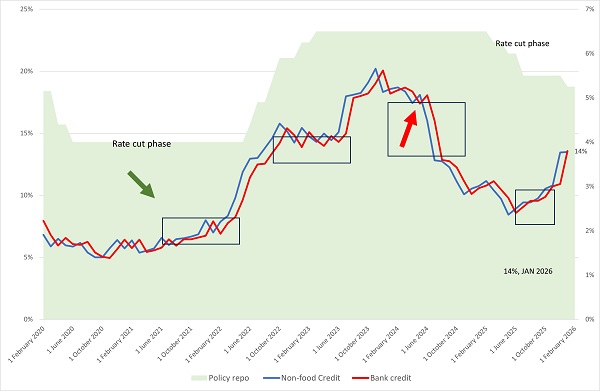

Source: RBI data, Authors’ annotations

This leads to the second concern: did the central bank miss crucial signals? Even if the monetary policy decided to keep the policy rate unchanged, keeping the stance unchanged seems overly optimistic. The importance of the stance lies in the forward-looking direction provided to the market. A sharper hawkish tone is expected to caution not only markets, but also firms and households through the credit transmission channel. Does this reflect a breakaway from recognising risks and using policy signalling effectively?

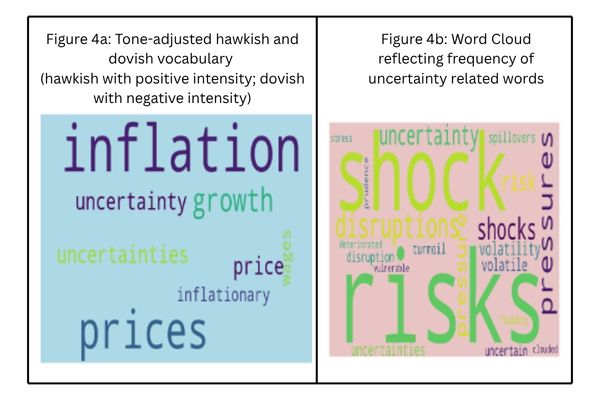

A reading of the MPC minutes deepens this concern. A simple analysis is presented here: Figure 4a presents the frequency count of inflation-sensitive (hawkish) terms in strengthening contexts and dovish terms in weakening contexts, while Figure 4b depicts the frequency count of uncertainty-related words. As the figures show, there is a much stronger focus on hawkish words than dovish ones, yet both the rate and stance remained unchanged. Uncertainty seems to be the underlying tone of discussion (figure 4b and Table 1), with little reflection in actual policy action.

Additionally, it needs to be iterated that there does not appear to have been a marked deterioration in credit conditions or growth indicators that would justify balancing inflation risks strongly enough to maintain a neutral stance.

If inflation indicators, imported price pressures, exchange-rate depreciation, and geopolitical risks were all pointing in the same direction, yet monetary policy decisions on rates or stance did not incorporate the upside skew in risks, the concern supersedes just that of delayed tightening.

Source: Authors’ calculations, Raw data: Monetary policy minutes

Table 1: Member wise uncertainty words usage (April Monetary policy minutes)

|

MPC Member |

Uncertainty-related word count |

Total words |

Frequency (count / total words) |

|

Dr. Nagesh Kumar |

6 |

643 |

0.93% |

|

Shri Saugata Bhattacharya |

18 |

710 |

2.54% |

|

Prof. Ram Singh |

20 |

872 |

2.29% |

|

Shri Indranil Bhattacharyya |

15 |

576 |

2.60% |

|

Dr. Poonam Gupta |

10 |

526 |

1.90% |

|

Shri Sanjay Malhotra* |

12 |

501 |

2.40% |

Raw data source: April Monetary policy minutes, *Governor, RBI has also highlighted uncertainty driven monetary policy decision making recently here

*Views are personal

More From BasisPoint