In 2007, I wrote a piece titled “Learning to Live with Impossible Trinity”. Back then, the Reserve Bank of India was facing an issue of massive foreign capital inflows powered by the ‘BRIC’ mania (Brazil, Russia, India, China) and the global credit boom.

The RBI was trying to prevent the rupee from appreciating and, in doing so, was accumulating foreign exchange reserves and, at the same time, infusing rupee liquidity into the system.

The then RBI governor, Y.V. Reddy, had admitted: “Dealing with the impossible trinity of fixed exchange rates, open capital accounts and discretion in monetary policy has become more complex than before”.

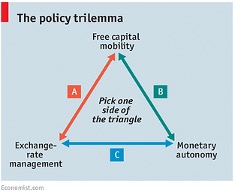

I found this very good image of the Impossible Trinity in The Economist magazine.

Indian monetary policy over the years has been muddling around the sides of this triangle at different points in time.

In 2007, one could argue the RBI was veering towards side A of the triangle in trying to manage the exchange rate from appreciating by using capital controls. However, the RBI even tried to kill the interest arbitrage by holding overnight rates at zero for a period and thus discouraging capital inflows. The money supply spike did cause a subsequent increase in inflation.

(The subsequent financial crisis of 2008 underscored the merit of the RBI in trying to discourage capital flows.)

In July 2013, troubled by the rapidly depreciating currency due to a high current account deficit, the RBI launched an exchange rate defence by tightening system liquidity and hiking overnight interest rates by 200 bps – a move towards side C of the triangle.

The currency fell even more after this move on growth concerns, and was stabilised only after durable capital flows were raised, and markets sought confidence from the words of the new RBI governor and from the announcement of Narendra Modi as the Prime Ministerial candidate for the Bharatiya Janata Party.

Learning from the episodes, India decided to adopt inflation targeting in 2015 as the main objective of monetary policy, with the Consumer Price Index Inflation as the nominal anchor. Under inflation targeting, the RBI’s monetary policy committee is solely focused on targeting CPI inflation in a 4% (+/-2%) band.

The RBI hasn’t really faced a tough inflation challenge in the last decade. There have been occasional short-term spikes in 2018 and 2022, and the volatility caused by COVID-19.

The RBI, to its credit, has remained true to this mandate to a large extent. India’s CPI inflation has remained well within its target range. However, the current situation may present the RBI with its toughest test on the objectives of monetary policy and its stance on managing growth, the external situation and the currency.

Rates vs Currency

Given the capital outflows seen since the start of 2025 and the rapidly depreciating currency, there have been growing calls for the RBI to act to ‘defend the currency’.

With the spread between the US and Indian interest rates, measured by the 10-year treasury yield, being at the lower end of its long-term band, many have voiced that Indian interest rates are not attractive enough in the current global context to draw in global capital flows. The expected response is to hike interest rates to make it attractive for foreign investors to invest in India's rate assets and thus increase capital inflows.

In its recent monetary policy announcement last week, the RBI not only held interest rates steady but also retained its stance as Normal. This was despite its projections for CPI inflation for 2026-27 rising to 5.1%.

The RBI sent a clear signal to the markets that it will remain true to its mandate of Inflation Targeting as the primary objective. It may increase interest rates to counter the increase in expected inflation, but it will do so in a calibrated manner after assessing the onset of monsoons and the trajectory of commodity prices.

For now, the RBI is not going to use interest rates to defend the currency. This is a crucial signal to the equity market investors. The RBI will not jeopardise growth by tightening interest rates and liquidity to defend the currency.

BOP - Toughest Challenge

However, the problem of capital inflows falling well short of the expected current account deficit, resulting in a balance of payments deficit, needs to be addressed. Between 2014 and 2024, low oil prices and adequate global capital inflows meant that India had a modest current account deficit and capital inflows were well in excess, allowing the RBI to build up substantial foreign exchange reserves.

That has now changed. Net Capital inflows are negative. And oil prices are near ~100$/bbl, just as they were during 2011-2013, which led to India being termed ‘Fragile Five’.

Some commentators have already labelled India – ‘Fragile Two’ or ‘Fragile One’, given India’s large currency depreciation over the last year, not only against the US dollar but even more against other OECD currencies and many emerging market currencies.

In the Impossible Trinity triangle, the RBI currently seems to be favouring side B – monetary autonomy and free capital flows.

Purists will argue that to not be true given the continued large intervention in the foreign exchange market to manage the value of the currency. Some will portend that it was RBI’s large two-sided intervention in late 2023 to mid-2024 to keep the Indian currency in a de-facto ‘peg’, that may have caused the eventual seemingly large depreciation since.

Rate Differential

Having decided to not hike interest rates to boost debt capital inflows, the RBI has decided to offer subsidies and tax benefits to attract global debt capital to fund the BOP deficit. With global dollar interest rates at ~4-5% and India interest rates at ~6-7%, and the cost of hedging at ~3%, it is a losing game to invest in India interest rate markets.

The RBI has, therefore, decided to

1) Subsidise the hedging cost for all FCNR Deposits till September 30, 2026. This will allow banks to offer, for example, a 6% dollar deposit to their clients, hedge it to rupee at zero cost and invest in rupee assets at ~7% to earn a risk-free spread of 1%. In 2013, a similar subsidy had raised ~$26 billion in FCNR (B) deposits from non-resident Indians. Given that the rate differentials are not as attractive as back then, the eventual inflow is unlikely to be substantial.

2) Subsidise the hedging cost of borrowings by PSUs in global bond markets. This may raise $5 billion to $10 billion. PSU’s offering 7%-dollar yields will be able to raise these amounts, but that is expensive and is subject to the extent of subsidy provided by the RBI.

The government has decided to reduce withholding tax and capital gains tax on foreign investments into Indian bond markets. The 20% withholding tax on interest and capital gains tax were significant deterrent to India bond investors. This is thus a welcome relief. India may see some small increase in allocations by some active emerging market bond funds, but this is unlikely to bring substantial inflows.

However, if this reduction in taxes is viewed favourably and if India is eventually included in the Bloomberg Global Bond indices, it would result in substantial ‘passive’ inflows from funds that track these indices. It will also lead to inflows from active funds that use these indices for performance benchmarking. This is indeed a big prospect, but it will not lead to any immediate inflows in the very near term.

If the RBI provides a cheaper hedging facility to even bond investors, either explicitly or by intervening in the forward markets to reduce the forward premia, it may trigger some hedged flows.

The BOP math

If oil prices remain elevated, the current account deficit over a 12-month period can rise to well above $70 billion.

The measures announced may bring in $20 billion-$30 billion. That still leaves a substantial inflow from FDI and FPI.

We can assume that net FDI inflows may improve given the slowdown in IPOs, and preferential offers by foreign companies / private equity/venture capital investors. FDI outflows by Indian companies/families could reduce given the sharp weakness in the Indian rupee. This may increase Net FDI numbers by about $20 billion-$30 billion.

Put together, we would be able to bridge the BOP deficit through the use of foreign exchange reserves.

Foreign Portfolio Investors can be a large swing flow; however, as of now, they remain net sellers given India’s lack of growth and earnings premium, no AI play, and relative valuations. India’s valuations on a relative basis are now saner than in 2024. The AI theme may face hiccups. If the West Asia conflict ends, it will remove the risk premia on key import commodities.

However, what India needs is:

1) Get back to double-digit nominal GDP , revenues, and earnings growth

2) Scrap Capital Gains Tax on Indian equity assets.

This can potentially lead FPIs to reinvest the $50 billion of net sales since 2024. The means to a solution to a ‘currency crisis’ is with the government.

The RBI has done its bit for now by not hiking interest rates and, at the same time, by trying to boost global debt flows.

.png)