.png)

Nilanjan Banik is a Professor at the School of Management, Mahindra University, specialising in trade, market structure, and development economics.

June 10, 2026 at 10:54 AM IST

The Indian economy, to quote Charles Dickens’ novel, looks like A Tale of Two Cities. Recent estimates suggest India's real GDP for the fourth quarter of FY26 expanded by 7.8%, with strong growth noted across sectors: services (9.3%), manufacturing (10.7%), and construction (7.4%).

What is worrying is that in recent times, the depreciation of the rupee has broken all earlier records. Among countries that are on a flexible exchange rate and not on a managed or fixed float — for example, Japanese Yen (6.6%), South Korean Won (7%), Indonesian Rupiah (9.3%), and the Philippine Peso (10.3%), to name a few — the Indian Rupee has depreciated the most over the last one year, by around 11.2%.

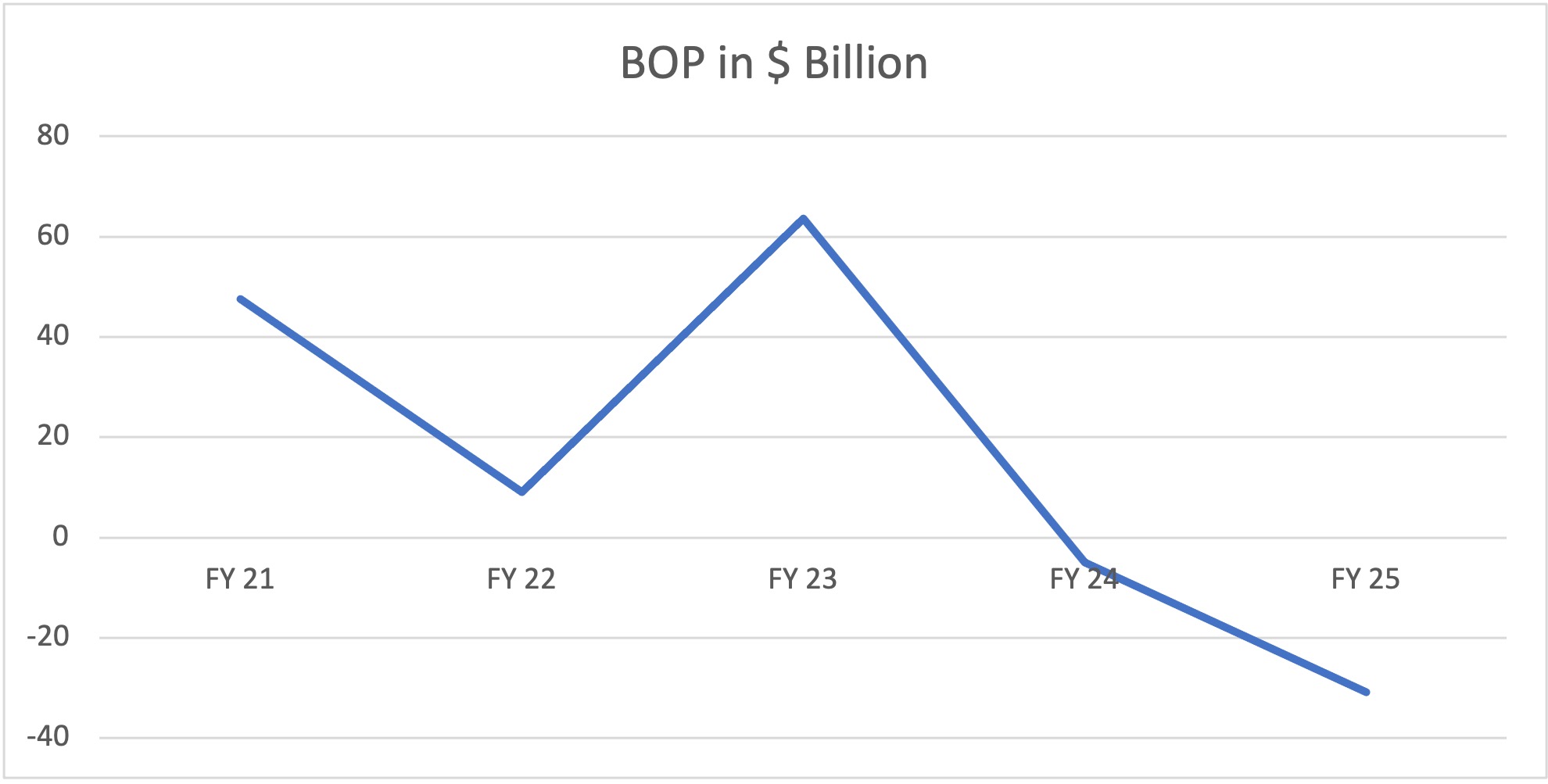

Source: RBI Annual Report 2025-26.

India has been importing crude oil worth $130 billion –$150 billion annually, and a significant portion of this import bill has been financed by the surplus in services, which has averaged over $240 billion during the past three years. For instance, during FY25, India’s overall merchandise trade deficit stood at $251.6 billion in FY25, down from $286.9 billion in the previous year.

However, this trend has changed in 2026. There are two major reasons. Indian stock market has been on a downward trend. FPIs pulled out money from India to the tune of Rs 2 lakh crore in FY26. The recent emergence of agentic AI models has raised concerns about the future of Indian software exports, which no longer appear as promising as before. Meanwhile, the US and Taiwanese stock markets are attracting renewed investor interest, driven by strong performance in microchip and AI stocks.

Second, the war in West Asia has also led to higher crude oil, fertiliser, and chemical product prices, adversely affecting India's external sector performance measured in terms of BOP. The war and higher price of imports have led to dollar appreciating against the Indian rupee, further worsening the CAD. India has to import almost 90% of its energy requirement. Every $10 rise in global Brent crude prices is estimated to widen India’s CAD by about 0.3% to 0.5% of GDP, translating to billions of dollars. Brent crude was trading between $66-$70 per barrel before the start of the war in February 2026, reaching to a high of $126 on 29 April 2026. Now, with UAE’s exit from OPEC, Brent crude may continue to hover around $80 a barrel for the remainder of 2026, even if Iran and the US decide to end the war. If the disruption persists through the rest the rest of 2026, Brent could average $91 per barrel in October-December of 2026.

Returning to the tale of two cities — for the Indian economy, the more consequential headwinds appear to be largely exogenous: geopolitical conflict and structural disruption of AI-driven automation, both of which lie beyond the government's direct control.

Where the government does have meaningful control, is in creating conditions that attract sustained FPI inflows, and make India a better place to do business. For instance, at the recent monetary policy meeting, the RBI outlined measures to simplify access for overseas investors to government bonds and equities. Separately, the government also announced a reduction in capital gains taxes on bond investments by FPIs.

The last time the government had initiated a bold reform measure was on September 20, 2019, when it reduced corporate taxes, slashing the base corporate income tax rate for domestic companies from 30% to 22%. The move was aimed at boosting domestic investment and reviving economic growth. However, larger corporates largely used the windfall not to reinvest within India, but to acquire foreign assets abroad. Corporate investment, by and large, remained subdued. This time, the focus needs to shift toward more targeted interventions — extending tax benefits or introducing interest subvention schemes for the MSME sector, strengthening incentives for setting up Global Capability Centers (GCCs), and deepening support for India's start-up ecosystem. Unlike the exogenous pressures the economy faces, these are firmly within the government's control, it only needs to deploy them wisely.

More From BasisPoint