.png)

June 26, 2025 at 2:07 AM IST

India’s financial markets now have a real-time mirror, and it is not the repo rate. In a quiet yet consequential move, economists at the Reserve Bank of India have developed a high-frequency Financial Conditions Index, compiled from twenty daily indicators across the money, bond, foreign exchange, equity, and corporate credit markets.

Unlike traditional metrics that offer lagged, narrow glimpses into market stress or exuberance, the new Financial Conditions Index distils India’s financial pulse into a single, dynamic number. Though published as a research article and not an official RBI policy document, it is part of the central bank’s broader effort to fine-tune its liquidity operations and rate signalling, especially as it seeks to distance monetary policy from episodic noise.

The timing is apt. As the RBI shifts toward using the Standing Deposit Facility as a corridor floor and relies increasingly on tools like variable-rate reverse repos to steer market rates, it needs a more comprehensive dashboard. The repo rate may remain unchanged for months, but financial conditions can shift rapidly. The Financial Conditions Index enables policymakers to measure that drift in near real-time.

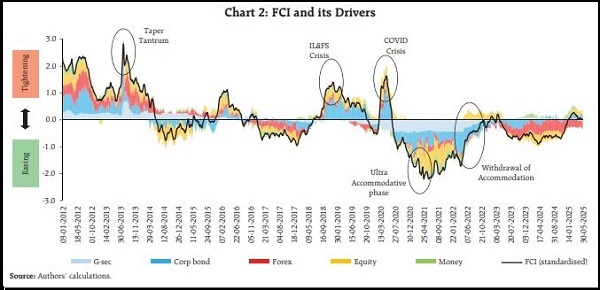

What stands out is the index’s construction. Rather than treat G-sec yields or the call money rate in isolation, the Financial Conditions Index accounts for slope and curvature of the yield curve, corporate bond spreads, VIX, forex volatility, and even P/E ratios relative to trend. It does not overweigh one market signal but integrates five asset classes into a single framework.

The index also has memory. Peaks in the Financial Conditions Index coincide with stress episodes like the 2013 taper tantrum, the IL&FS collapse, and the March 2020 COVID crash. Its latest reading suggests that conditions, after tightening briefly post-US election results in late 2024, are now close to neutral, thanks to buoyant equity markets and surplus system liquidity.

Market filter

This has direct implications for bond traders and those monitoring liquidity. If short-end rates are rising due to cash crunches, but the Financial Conditions Index remains easy, it implies the RBI may hold off from intervention. Conversely, if the repo rate is stable but the Financial Conditions Index tightens due to widening credit spreads or foreign exchange volatility, it could foreshadow regulatory or liquidity responses.

The market often focuses on the RBI’s stance—accommodative, neutral, or hawkish—but that single-word label increasingly masks complexity. Financial conditions are shaped as much by sentiment and global spillovers as they are by policy intent. A tool like the Financial Conditions Index allows both the central bank and markets to see how these forces interact.

Globally, central banks have long embedded Financial Conditions Indices into their models. The US Federal Reserve, the ECB, and the Bank of Canada all reference them to assess policy traction. India’s belated adoption of a high-frequency Financial Conditions Index, even as a research output, reflects both a maturing policy ecosystem and the technological readiness to process market data daily.

What comes next is just as interesting. The RBI is likely to explore using the Financial Conditions Index as a lead indicator for economic activity, and early findings from the article suggest it has predictive power over industrial output. That could influence the timing of policy moves, particularly when lagging indicators like inflation or GDP growth paint a conflicting picture.

It also has potential value in stress testing financial stability. If certain markets like mid-cap equities or the corporate bond segment disproportionately tighten financial conditions, the RBI could adjust macroprudential norms or liquidity provisioning accordingly.

For now, the Financial Conditions Index remains an academic artefact. It is neither referenced in policy statements nor widely tracked by market participants. That will likely change. As liquidity frictions re-emerge and rate policy enters a long hold, tools like the Financial Conditions Index could become central to how we understand the RBI’s next move, not by what it says, but by what it sees.

More From BasisPoint